Highlights:

- Why holding 8 ETFs often gives the same returns as holding 3

- The hidden “complexity tax” that doesn’t show up on any statement

- How to simplify your portfolio without triggering capital gains

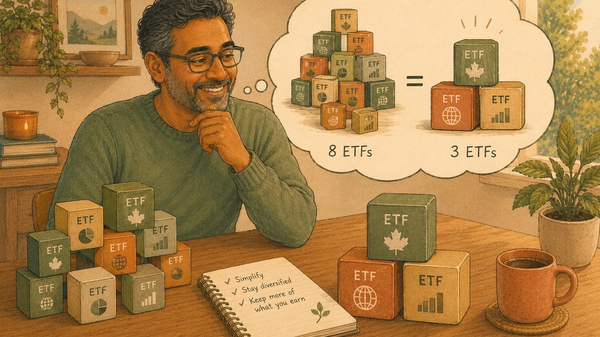

A portfolio that holds 3 or 8 ETFs can deliver nearly identical returns over 30 years. So why are so many DIY investors holding funds they don't actually need?

If your portfolio has more funds than you can explain in one sentence, this piece breaks down why extra ETFs rarely add diversification - and how to tell if your portfolio has a design problem hiding in plain sight.

The portfolio that grew to 8 ETFs

Most passive investors never set out to build a complicated portfolio. It happens gradually.

You start with a Canadian equity ETF, an international one, and a bond fund. Clean and simple. Then you read about U.S. market exposure and add a separate S&P 500 ETF.

Then someone mentions emerging markets, so you add that. Then you hear about REITs for real estate exposure. Then a small-cap fund. Then a separate Canadian dividend ETF for income.

Suddenly you’re holding 8 ETFs across three accounts and you can’t remember why half of them are there.

Here’s what most people don’t realize: a portfolio of 3 broad index ETFs - say, a Canadian equity ETF, an international equity ETF, and a bond ETF - already holds thousands of individual stocks and bonds. You’re already diversified across 40+ countries and every major sector.

In many cases, that eighth ETF doesn’t meaningfully add diversification. It mostly adds another line item.

The complexity tax is a design problem

When people talk about the "cost" of investing, they usually mean MERs and trading commissions. But there's another cost that doesn't show up on any statement.

Call it the complexity tax. It's what happens when your portfolio has more moving parts than it actually needs.

If you're using Passiv, the rebalancing math is already taken care of - target weights, contribution splits, drift notifications. That part's handled.

But here's what even good automation can't change: when you're contributing $500 a month across 8 ETFs, some of those positions are getting $30 or $50 at a time.

At that size, your money isn't really moving the needle on any single holding. You're spreading contributions so thin that individual positions barely shift.

With 3 ETFs, every contribution lands with purpose. A $500 deposit split three ways puts $150-$200 into each fund. That's enough to meaningfully bring a drifted position back toward target in a single contribution.

Fewer funds doesn't just mean less to manage. It means every dollar you invest is actually doing something.

That's good portfolio design.

The overlap problem nobody checks

This is the part that surprises people.

If you’re holding a broad Canadian equity ETF like XIC and a Canadian dividend ETF like XDV, you’ve got significant overlap. The top holdings in both funds are the same banks and energy companies. You’re not more diversified - you’re double-counting.

The same thing happens when people hold XEQT (which already includes Canadian, U.S., international, and emerging-market stocks) and add a separate U.S. S&P 500 ETF on top. You’re now overweight U.S. stocks without necessarily realizing it.

A well-designed 3-ETF portfolio mostly avoids this. Each fund covers a distinct slice with minimal overlap.

What a clean 3-ETF portfolio actually looks like

For most Canadian DIY investors, a simple portfolio looks something like this:

A Canadian equity ETF (like XIC or VCN) for domestic exposure. An international equity ETF (like XAW or VXC) for everything outside Canada. A bond ETF (like ZAG or VAB) for stability.

That’s it. Three funds. Thousands of underlying holdings. Global diversification.

Your allocation between them depends on your age, risk tolerance, and timeline. A younger investor might go 40/50/10. Someone closer to retirement might hold more bonds at 30/30/40. The point is that three funds can cover virtually any allocation you’d need.

Simplifying without creating tax problems

If you’re already holding 6 or 8 ETFs and you want to simplify, the path depends on which accounts they’re in.

In your RRSP, TFSA, or RESP, it’s straightforward. You can sell and rebuy without triggering taxes inside those accounts.

Many investors consolidate over a month or two - sell the duplicates, fold the small positions into the core 3 funds, and you’re done.

In a non-registered (taxable) account, selling can trigger capital gains. The patient approach: stop adding to the small positions, direct all new contributions to your core 3 ETFs, and let the extras get diluted over time. You don’t need to rip everything apart at once.

If you have positions that are sitting at a loss, you can actually use that to your advantage. Selling at a loss lets you claim the capital loss against gains elsewhere. Just be aware of the superficial loss rule - you can’t rebuy the same fund (or a substantially identical one) within 30 days before or after the sale.

The real cost of “just one more ETF”

Every additional ETF in your portfolio adds friction in ways that are easy to underestimate.

The more funds you hold, the more decisions you have to make - and the more opportunities you have to talk yourself out of your own plan.

Complexity can hurt the most when markets are rocky. At the bottom of a bear market, a portfolio you can explain in one sentence - “I hold Canadian stocks, international stocks, and bonds” - is a portfolio you can stick with. A portfolio with 8 funds across three accounts can give you a lot more reasons to second-guess yourself.

Simplicity isn’t just easier to manage - it’s easier to trust.

You’ve already done the hard part

If you’ve been contributing consistently, staying in the market, and not panic-selling during downturns, you’ve already done the things that actually matter.

The number of ETFs in your portfolio? For most investors, it matters far less than your savings rate and your ability to stay the course.

So if you’ve been wondering whether your 3-fund portfolio is “enough” - it is. And if you’re holding 8 funds and feeling overwhelmed, you have permission to simplify.

Good investing is easier than it seems.

Whether you’re consolidating from 8 ETFs down to 3 or keeping your current setup running smoothly, Passiv Elite takes the rebalancing math off your plate entirely.

Set your target allocation once, and Elite calculates your trades automatically - across your RRSP, TFSA, RESP, and non-registered accounts in one household view.

When it’s time to rebalance, place every trade with a single click instead of logging into each account and doing the math yourself. Try Passiv Elite and get your time back.